Authors:

Preeti Wadhwani, Satyam Jaiswal

Download free PDF

Software-Defined Vehicle Market Size & Share 2026-2035

Report ID: GMI6887

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Software-Defined Vehicle Market

Get a free sample of this report

Get a free sample of this report Software-Defined Vehicle Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

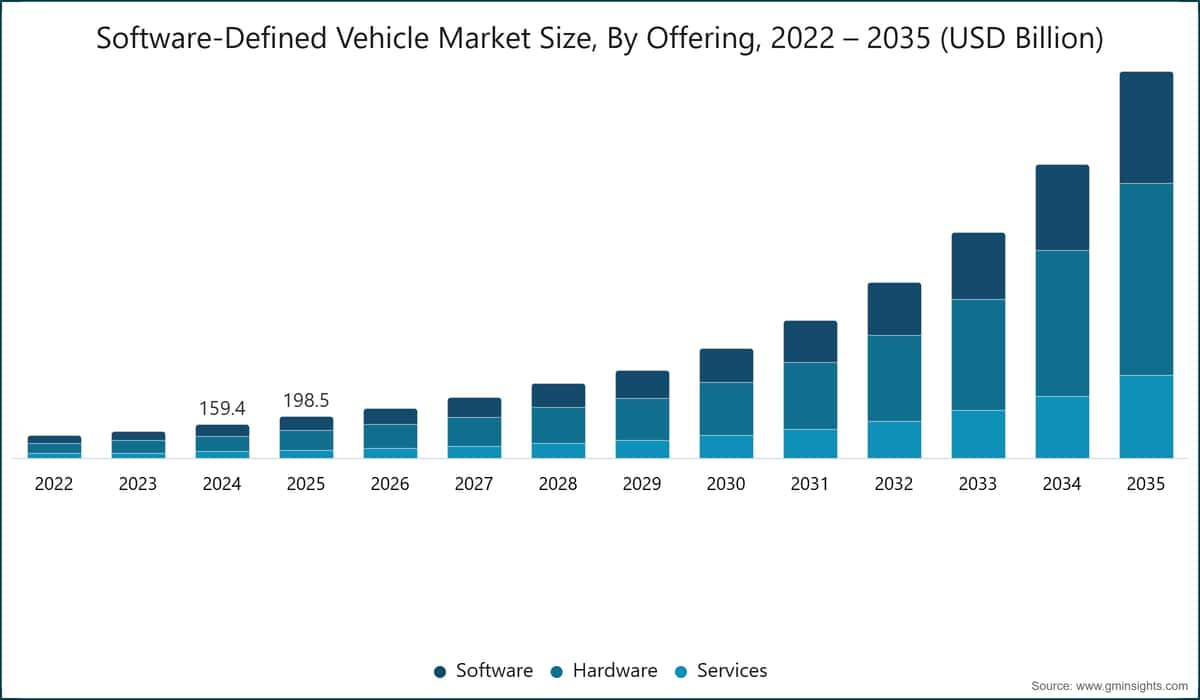

Software-Defined Vehicle Market Size

The global software-defined vehicle market was valued at USD 198.5 billion in 2025. The market is expected to grow from USD 239.5 billion in 2026 to USD 1,864.1 billion in 2035 at a CAGR of 25.6%, according to latest report published by Global Market Insights Inc.

Software-Defined Vehicle Market Key Takeaways

Market Leader: Tesla led with over 8.5% market share in 2025.

Leading Players: Top 5 players in this market include Tesla, BYD, Mercedes-Benz Group, Zeekr, Li Auto, which collectively held a market share of 25.9% in 2025.

The software-defined vehicle (SDV) market is undergoing a structural transformation in 2026, evolving from fragmented automotive software development environments into integrated, cloud-native vehicle software ecosystems that support continuous software engineering, machine learning operations (MLOps), and over-the-air (OTA) deployment. This transition is being driven by the adoption of software-defined vehicle architectures, increasing integration of artificial intelligence (AI) and machine learning (ML) into automotive systems, and the need for end-to-end orchestration of development, testing, validation, and deployment workflows across OEMs and Tier-1 suppliers. Software-Defined Vehicles are becoming a central intelligence layer in modern mobility, enabling real-time data processing, simulation-based validation, and continuous delivery of automotive applications across the vehicle lifecycle.

Regulatory and industry frameworks are accelerating the adoption of Software-Defined Vehicles across global automotive ecosystems. In Europe, UNECE R155 and R156 regulations are enforcing cybersecurity and software update management requirements, encouraging OEMs to adopt traceable and auditable DevOps pipelines. In the United States, the National Highway Traffic Safety Administration (NHTSA) and related mobility initiatives are supporting connected vehicle safety systems, autonomous driving validation frameworks, and digital compliance architectures enabled through cloud analytics, MLOps, and AI-based monitoring systems. In Asia-Pacific, governments in China, Japan, and India are promoting intelligent vehicle infrastructure, electric vehicle expansion, and smart mobility frameworks that support large-scale cloud-native automotive software deployment.

Real-world deployment of software-defined vehicle market is expanding across global OEMs and technology ecosystems. Automotive players such as Volkswagen Group (CARIAD), BMW, Mercedes-Benz Group, General Motors (Ultifi), and Tesla are integrating centralized software platforms to enable OTA updates, AI model deployment, vehicle telemetry processing, and continuous feature upgrades. Technology providers such as Amazon Web Services, Microsoft Azure, Google Cloud, NVIDIA, Databricks, and Snowflake are enabling automotive cloud ecosystems that support simulation environments, digital twins, large-scale data processing, and machine learning lifecycle management.

From a regional perspective, North America leads SDV adoption due to strong hyperscaler ecosystems, advanced AI infrastructure, and early deployment of software-defined vehicle platforms. Europe follows with a regulation-driven transformation, supported by Germany’s strong automotive software ecosystem and compliance-led vehicle lifecycle management systems. Asia-Pacific represents the fastest-growing region, driven by rapid electric vehicle expansion, strong SDV adoption in China, Japan, and South Korea, and increasing cloud-native automotive development in India. Latin America and the Middle East & Africa remain emerging regions, with adoption primarily concentrated in fleet digitization, connected mobility services, and early-stage automotive analytics and telematics deployment.

Software-Defined Vehicle Market Trends

The software-defined vehicle (SDV) market is being shaped by the rapid shift toward software-defined architectures, where vehicles are increasingly treated as continuously upgradable software platforms rather than static hardware products. This is driving strong demand for cloud-native DevOps pipelines and MLOps frameworks that enable continuous integration, testing, deployment, and monitoring of automotive software and AI models across the vehicle lifecycle.

A major trend is the convergence of DevOps and MLOps into unified automotive software lifecycle platforms. OEMs and Tier-1 suppliers are increasingly adopting integrated environments that combine software development, simulation, data engineering, and AI model training within a single cloud-based workflow. This helps reduce development cycles, improve software reliability, and accelerate deployment of new vehicle features across global fleets. Another key trend is the growing importance of AI-driven autonomy and advanced driver-assistance systems (ADAS), which is increasing the need for large-scale machine learning model training and validation. This is driving adoption of MLOps platforms that support real-world driving data ingestion, synthetic simulation environments, and continuous model retraining at fleet scale to improve safety, accuracy, and performance.

The expansion of over-the-air (OTA) software update ecosystems is also reshaping the market. Automotive companies are moving toward continuous delivery models where vehicle software is updated remotely throughout the lifecycle, requiring robust DevOps pipelines, version control systems, and cloud orchestration layers to ensure secure, seamless, and reliable software deployment. Another key trend is the exponential growth of connected vehicle data, which is transforming automotive software architecture. Modern vehicles generate large volumes of sensor, telemetry, and behavioral data, creating strong demand for scalable cloud data platforms capable of real-time processing, storage, and analytics. This data is increasingly used for predictive maintenance, fleet optimization, and safety monitoring.

Regulatory compliance and cybersecurity requirements are further accelerating adoption. Standards such as UNECE R155 and R156 are forcing OEMs to implement secure software update mechanisms, audit trails, and controlled deployment pipelines. This is strengthening the need for enterprise-grade DevOps and MLOps governance frameworks across the automotive software ecosystem.

Hyperscaler ecosystems are playing a central role in market expansion, with providers such as Amazon Web Services, Microsoft Azure, and Google Cloud enabling end-to-end automotive cloud infrastructure. At the same time, companies such as NVIDIA and Databricks are supporting simulation, AI training, and large-scale model deployment. The market is increasingly shifting toward platform consolidation, where OEMs and suppliers move away from fragmented toolchains toward integrated automotive cloud ecosystems that unify DevOps, MLOps, simulation, and data management into a single operational layer.

Software-Defined Vehicle Market Analysis

Based on offering, the software-defined vehicle (SDV) market is segmented into Software, Hardware, and Services. Hardware dominated the market, accounting for 47% in 2025 and are expected to grow at a CAGR of 26.3% through 2026 to 2035.

Based on propulsion, the software-defined vehicle market is segmented into Internal Combustion Engine (ICE) Vehicles, Electric Vehicles (EVs), and Hybrid Vehicles. Internal Combustion Engine (ICE) Vehicles segment dominates the market with 37.6% share in 2025, and the segment is expected to grow at a CAGR of 17.9% from 2026 to 2035.

Based on E/E architecture, the software-defined vehicle market is segmented into distributed architecture, domain centralized architecture, zonal architecture, and hybrid architecture. Distributed Architecture segment dominates the market with 50.7% share in 2025.

Based on application, the software-defined vehicle market is segmented into advanced driver assistance systems (ADAS) & autonomous driving, infotainment systems / digital cockpit, telematics & connectivity, powertrain management, body control & comfort systems, fleet management, and others. Infotainment Systems / Digital Cockpit segment is expected to dominate the market with a share of 27.2% in 2025.

China dominates the Asia Pacific software-defined vehicle market accounting for 57% and generating USD 41.4 billion in 2025.

US dominates North America software-defined vehicle market growing with a CAGR of 22.6% from 2026 to 2035.

Germany dominates the Europe software-defined vehicle market, showcasing strong growth potential, with a CAGR of 25.1% from 2026 to 2035.

Brazil leads the Latin American software-defined vehicle market, exhibiting remarkable growth of 28.9% during the forecast period of 2026 to 2035.

UAE witnessed substantial growth in the Middle East and Africa software-defined vehicle market in 2025.

Software-Defined Vehicle Market Share

Software-Defined Vehicle Market Companies

Major players operating in the software-defined vehicle industry are:

8.5% market share

Collective market share in 2025 is 25.9%

Software-Defined Vehicle Industry News

In May 2026, BYD announced advancements in its proprietary autonomous driving chip architecture under its “God’s Eye” system, strengthening its vertically integrated software-defined vehicle (SDV) stack. The development enhances in-house AI computing capabilities for real-time driving intelligence, OTA updates, and advanced driver assistance systems across its EV portfolio.

In May 2026, BYD expanded the deployment of its assisted-driving ecosystem across multiple vehicle segments, accelerating the integration of AI-powered driving functions and continuous software updates. The initiative reflects the company’s broader strategy to scale SDV capabilities through deep hardware–software integration and cloud-connected vehicle platforms.

In August 2025, XPeng released its XOS 5.8.0 over-the-air software update, introducing enhanced driver-assistance features, AI-based personalization, and improved co-driving capabilities. The update reinforces XPeng’s SDV approach, centered on continuous software iteration and cloud-connected vehicle intelligence.

In January 2025, XPeng launched its XOS 5.4 global OTA update, improving smart driving functions, safety systems, and in-vehicle AI interaction features. The rollout highlights the company’s strategy of frequent software upgrades to strengthen its software-defined vehicle ecosystem.

In March 2024, NVIDIA expanded its automotive AI partnerships with leading electric vehicle manufacturers, including BYD and XPeng, to accelerate the development of next-generation autonomous driving platforms. The collaboration strengthens NVIDIA’s role in providing high-performance compute and AI infrastructure for SDV architectures.

The software-defined vehicle market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue (USD Bn) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Offering

Market, By Propulsion

Market, By E/E Architecture

Market, By SDV Maturity Level

Market, By Application

Market, By Vehicle

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Research Methodology

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Offering, 2022 - 2035 (USD Bn)

Chapter 6 Market Estimates & Forecast, By E/E Architecture, 2022 - 2035 (USD Bn, Units)

Chapter 7 Market Estimates & Forecast, By SDV Maturity Level, 2022 - 2035 (USD Bn, Units)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Bn)

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 (USD Bn, Units)

Chapter 10 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Bn, Units)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Bn, Units)

Chapter 12 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →