Summary

Table of Content

Metalworking Fluids Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Metalworking fluids Market Size

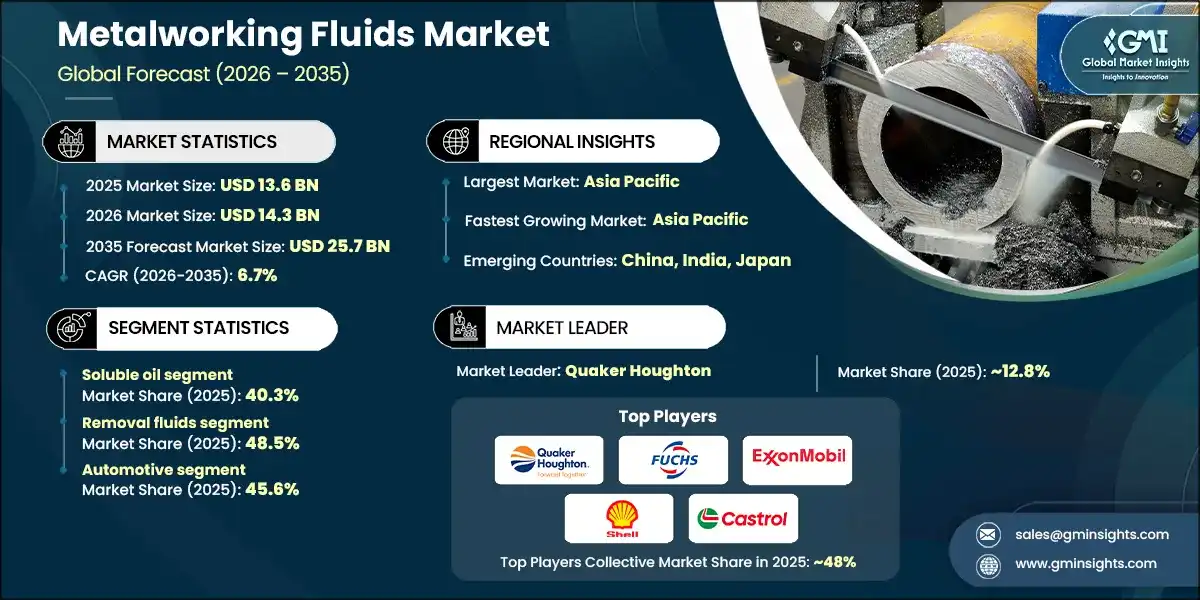

The global metalworking fluids market was valued at USD 13.6 billion in 2025. The market is expected to grow from USD 14.3 billion in 2026 to USD 25.7 billion in 2035, at a CAGR of 6.7%, according to latest report published by Global Market Insights Inc.

To get key market trends

- Metalworking fluids are specialized lubricants and coolants used in metal cutting, grinding, forming, and surface treatment operations across manufacturing industries. Available in various formulations including neat oils (straight cutting oils), soluble oils (emulsifiable concentrates), semi-synthetic fluids (hybrid formulations), and fully synthetic fluids, these performance-critical products provide essential functions including heat dissipation, friction reduction, chip removal, corrosion protection, and tool life extension in metalworking operations.

- Currently, Asia Pacific dominates the metalworking fluids market, accounting for approximately 44.8% of global market value in 2025, driven by extensive automotive manufacturing capacity, robust machinery production, and expanding aerospace fabrication facilities. North America represents a significant market with established manufacturing infrastructure, while Europe maintains substantial market presence with advanced automotive and aerospace industries requiring high-performance metalworking solutions.

- Removal fluids (cutting and grinding applications) represent the largest application segment, accounting for approximately 48.5% of the market, reflecting the dominant role of machining operations in metal fabrication globally, followed by forming fluids, protecting fluids, and treating fluids. Among product types, soluble oil leads with approximately 40.3% market share, followed by semi-synthetic fluids, synthetic fluids, and neat oils, reflecting the widespread adoption of water-miscible formulations offering balanced performance and cost-effectiveness.

- The convergence of expanding automotive production, growing aerospace manufacturing, and advancing metalworking technologies creates a dynamic environment for the global metalworking fluids market. As manufacturers invest in advanced formulation technologies, bio-based and sustainable products, and performance optimization for high-speed machining, the market continues to evolve, ensuring sustained global demand across diverse manufacturing sectors and geographic markets.

Metalworking Fluids Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 13.6 billion |

| Market Size in 2026 | USD 14.3 billion |

| Forecast Period 2026 - 2035 CAGR | 6.7% |

| Market Size in 2035 | USD 25.7 billion |

| Key Market Trends | |

| Drivers | Impact |

| Expanding automotive production capacity globally | Driving substantial metalworking fluids consumption as automotive manufacturing remains the dominant end-use sector, supporting machining, forming, and assembly operations across engine components, transmission systems, chassis parts, and body panels in passenger vehicles and commercial transportation industries |

| Growing aerospace manufacturing & defense spendin | Increasing demand for high-performance metalworking fluids for precision machining of titanium alloys, aluminum aerospace grades, and superalloys, driven by commercial aircraft production ramp-ups, defense modernization programs, and stringent quality requirements in aerospace component fabrication |

| Advanced machining technologies & high-speed operations | Expanding metalworking fluids applications in CNC machining centers, multi-axis turning operations, and high-speed grinding systems, driven by Industry 4.0 adoption, automation advancement, and technical requirements for extreme pressure lubrication and thermal management in modern manufacturing environments |

| Pitfalls & Challenges | Impact |

| Environmental regulations & worker health concerns | Create compliance challenges for producers and end-users, requiring investment in bio-based formulations, low-mist technologies, waste treatment systems, and comprehensive health & safety programs across manufacturing facilities globally |

| Shift toward dry machining & minimum quantity lubrication (MQL) | Creates competitive pressure from alternative metalworking technologies reducing fluid consumption, potentially affecting traditional flood cooling applications and requiring product innovation for micro-lubrication and near-dry machining systems |

| Opportunities: | Impact |

| Bio-based & sustainable formulation development | Offers opportunities for premium positioning in environmentally conscious manufacturing operations, enabling market differentiation through renewable raw materials, biodegradability, reduced toxicity, and improved worker safety profiles addressing regulatory and corporate sustainability requirements |

| Digitalization & fluid management systems | Present significant growth potential through IoT-enabled monitoring, predictive maintenance, concentration control automation, and data analytics for fluid performance optimization, enabling value-added services, extended fluid life, and total cost of ownership reduction for manufacturing customers |

| Market Leaders (2025) | |

| Market Leaders |

12.8% market share |

| Top Players |

|

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest growing market | Asia Pacific |

| Emerging country | China, India, Japan |

| Future outlook |

|

What are the growth opportunities in this market?

Metalworking fluids Market Trends

- Advanced formulation technologies and performance optimization are revolutionizing metalworking fluids development, enabling producers to achieve superior lubricity characteristics, enhanced thermal stability, extended sump life, and improved surface finish quality across diverse machining operations. These technological improvements address critical requirements for high-speed machining, hard metal processing, and precision grinding applications in automotive, aerospace, and general engineering sectors, significantly enhancing tool life, reducing cycle times, and improving dimensional accuracy through optimized additive packages, base fluid selection, and emulsion stability technologies.

- The sustainability transformation is reshaping the metalworking fluids industry as manufacturers demonstrate increasing commitment to environmental responsibility through bio-based formulations, reduced hazardous substance content, and circular economy initiatives including fluid recycling and waste minimization programs. This shift encourages investment in renewable raw materials, biodegradable additives, and low-toxicity formulations, with several major producers implementing comprehensive product stewardship programs to address regulatory requirements regarding worker exposure limits, wastewater treatment, and disposal regulations, while meeting stakeholder expectations for sustainable manufacturing practices and reduced environmental footprint.

- Strategic partnerships between fluid manufacturers, machine tool builders, and end-user manufacturing facilities are creating integrated metalworking solutions and optimizing operational efficiency across the manufacturing ecosystem. These collaborative relationships enable coordinated product development with machine tool specifications, application-specific formulation optimization, and comprehensive fluid management services including monitoring, maintenance, and performance analytics, positioning integrated solution providers with competitive advantages in technical service capabilities, total cost of ownership reduction, and long-term customer relationships compared to commodity fluid suppliers.

- Geographic capacity expansion in Asia Pacific, particularly in China, India, Vietnam, and Thailand, is fundamentally reshaping global metalworking fluids supply dynamics, with significant production capacity additions and technical service infrastructure development supporting rapidly growing regional automotive manufacturing, machinery production, and aerospace component fabrication industries. These investments reduce import dependence for regional manufacturers, improve supply chain responsiveness, and enable closer technical collaboration with automotive OEMs, tier suppliers, and contract manufacturers in high-growth markets, while creating competitive pressure on established North American and European producers.

- Product specialization and application-specific formulation development are emerging as critical differentiation strategies, with producers expanding beyond general-purpose metalworking fluids to offer specialized products for titanium machining, aluminum aerospace alloys, hardened steel grinding, and advanced materials processing. This trend addresses evolving requirements in aerospace component manufacturing, automotive lightweighting initiatives, and precision engineering applications, enabling premium pricing and stronger customer relationships through customized formulations, technical application support, and collaborative problem-solving with manufacturing engineers in automotive, aerospace, and industrial machinery sectors.

Metalworking Fluids Market Analysis

")

Learn more about the key segments shaping this market

Based on product, the market is segmented into neat oil, soluble oil, semi-synthetic fluid, and synthetic fluid. Soluble oil dominated the market with an approximate market share of 40.3% in 2025 and is expected to grow with a CAGR of 6.5% from 2026 to 2035.

- Soluble oil dominates due to its optimal balance between lubrication performance, cooling efficiency, and cost-effectiveness for general machining operations, providing excellent emulsion stability, versatile application suitability, and proven performance across turning, milling, drilling, and grinding operations. This product type provides superior heat dissipation through water-based emulsions while maintaining adequate boundary lubrication for moderate-duty metalworking operations. Its established position in automotive component manufacturing, general engineering workshops, and machinery production facilities, coupled with proven compatibility with diverse metal substrates and machining processes, solidifies its leading market position across manufacturing regions globally.

- Synthetic fluid represents the fastest-growing segment with a CAGR of 7.3% from 2026 to 2035, driven by superior performance characteristics including extended sump life, excellent biological stability, superior cooling properties, and reduced maintenance requirements compared to conventional oil-based formulations. Advanced synthetic formulations enable operation in demanding applications requiring tight tolerances, high-speed machining, and difficult-to-machine materials including titanium, stainless steel, and heat-resistant alloys. Growing adoption in aerospace manufacturing, automotive precision machining, and high-value component fabrication, coupled with total cost of ownership advantages through reduced fluid consumption and extended replacement intervals, drive accelerating market penetration, particularly in developed markets with advanced manufacturing operations.

- Semi-synthetic fluid occupies a significant segment with 39.2% market share in 2025, serving applications requiring performance characteristics between soluble oils and synthetic fluids, combining mineral oil lubricity with synthetic fluid stability and cooling efficiency. This product type provides enhanced performance for moderate-to-heavy duty machining operations, improved biological resistance compared to straight soluble oils, and cost advantages versus fully synthetic formulations. Its established market presence in automotive manufacturing, aerospace component machining, and general metalworking operations maintains robust demand supported by a CAGR of 6.6% through 2035, driven by balanced performance-to-cost ratios and versatility across diverse machining applications requiring enhanced capabilities beyond conventional soluble oils.

")

Learn more about the key segments shaping this market

Based on application, the metalworking fluids market is segmented into removal fluids, forming fluids, protecting fluids, and treating fluids. Removal fluids dominated the market with an approximate market share of 48.5% in 2025 and is expected to grow with a CAGR of 7.2% from 2026 to 2035.

- Removal fluids dominate due to the fundamental importance of cutting, grinding, milling, drilling, and turning operations in metal fabrication processes, representing the largest metalworking operation category globally across automotive manufacturing, aerospace component production, and general engineering sectors. This application encompasses the broadest range of machining operations requiring specialized lubrication, cooling, chip removal, and tool protection functions essential for productive metal removal processes. Its fundamental role in manufacturing value chains, coupled with continuous expansion of machining capacity in automotive and aerospace industries, solidifies its leading market position with strong growth driven by increasing manufacturing output and advanced machining technology adoption.

- Removal fluids also represent the fastest-growing segment with a CAGR of 7.2% from 2026 to 2035, driven by expanding automotive production capacity, aerospace manufacturing growth, and increasing adoption of high-speed machining technologies requiring advanced fluid performance for thermal management and tool life optimization. Technological advancement in CNC machining centers, multi-axis turning operations, and precision grinding systems creates growing demand for high-performance removal fluids supporting extreme cutting speeds, hard metal machining, and tight tolerance requirements. Increasing manufacturing complexity, expanding production of electric vehicle components, and growing aerospace component fabrication drive accelerating consumption, particularly in Asia Pacific markets with rapid automotive and aerospace manufacturing expansion.

- Forming fluids occupy a significant segment with 29.8% market share in 2025, serving metal forming operations including stamping, drawing, rolling, forging, and extrusion processes requiring specialized lubrication for metal deformation without cutting. This application provides essential boundary lubrication, die protection, and surface finish control for sheet metal forming, tube bending, and bulk metal forming operations across automotive body panel production, appliance manufacturing, and structural component fabrication. Its established position in automotive stamping plants, metal forming job shops, and appliance manufacturing facilities maintains steady consumption supported by a CAGR of 6.3% through 2035, driven by automotive production growth and expanding metal forming capacity in emerging manufacturing markets.

Based on end-use, the metalworking fluids market is segmented into automotive, aerospace, construction, electrical & power, agriculture, marine, healthcare, and others. Automotive dominated the market with an approximate market share of 45.6% in 2025 and is expected to grow with a CAGR of 7.2% from 2026 to 2035.

- Automotive dominates due to the industry's massive metalworking operations spanning engine component machining, transmission manufacturing, chassis fabrication, body panel stamping, and precision component production requiring extensive metalworking fluids consumption across cutting, grinding, forming, and surface treatment operations. This end-use sector represents the largest single consumer of metalworking fluids globally, with established automotive manufacturing infrastructure consuming substantial fluid volumes across powertrain production, vehicle assembly operations, and tier supplier component fabrication. Its fundamental importance in global manufacturing, coupled with expanding electric vehicle production and continuous automotive capacity additions in emerging markets, solidifies its leading market position with robust growth driven by automotive industry expansion in Asia Pacific regions.

- Aerospace represents the fastest-growing segment with a CAGR of 7.5% from 2026 to 2035, driven by commercial aircraft production ramp-ups, defense spending increases, and expanding aerospace component manufacturing requiring specialized high-performance metalworking fluids for titanium machining, aluminum aerospace alloy processing, and superalloy grinding operations. Advanced aerospace manufacturing demands exceptional fluid performance for precision tolerances, difficult-to-machine materials, and stringent quality requirements including cleanliness standards and traceability documentation. Growing commercial aviation demand, defense modernization programs, and expanding aerospace manufacturing capacity in emerging markets drive accelerating consumption, particularly for premium synthetic and semi-synthetic formulations meeting aerospace industry specifications and OEM approvals.

- Electrical & power occupies a significant segment with 12.8% market share in 2025, utilizing metalworking fluids for manufacturing electrical equipment, power generation components, transformer parts, motor housings, and precision electrical components requiring specialized machining and forming operations. This end-use sector leverages metalworking fluids for copper and aluminum processing, electrical steel lamination production, and precision component fabrication supporting power infrastructure, renewable energy equipment, and electrical machinery manufacturing. Its established position in electrical equipment manufacturing, power generation infrastructure development, and industrial motor production maintains steady demand supported by a CAGR of 6.0% through 2035, driven by electrical infrastructure expansion, renewable energy growth, and increasing electrification across industrial and transportation sectors globally.

")

Looking for region specific data?

The U.S. metalworking fluids market accounted for USD 2.6 billion in 2025.

- The strong momentum for metalworking fluids in North America comes primarily from the United States, wherein consistent demand is driven by well-established automotive manufacturing facilities consuming removal fluids for engine component machining and transmission production, extensive aerospace component fabrication infrastructure requiring high-performance synthetic and semi-synthetic fluids for titanium and aluminum alloy processing, and robust machinery manufacturing sector utilizing forming fluids for metal stamping operations. Constant emphasis on manufacturing modernization and reshoring initiatives, sophisticated metalworking operations producing precision automotive and aerospace components, and established fluid management capabilities consistently elevate the country's market position. The presence of major producers including Quaker Houghton, ExxonMobil, and Chevron ensures sustained supply and market leadership.

The metalworking fluids market in Germany is estimated to experience significant and promising growth from 2026 to 2035.

- Metalworking fluids growth in Europe is integral due to strong automotive manufacturing heritage, mature aerospace component production capabilities, and well-established precision machinery fabrication. In Germany, producers focus on high-performance semi-synthetic and synthetic formulations meeting stringent specifications for automotive powertrain machining, bio-based products addressing REACH regulations, and specialty fluids for aerospace titanium processing and hardened steel grinding. Germany's leadership in automotive engineering and precision manufacturing, combined with premium automotive production, aerospace component fabrication requiring advanced removal fluids, and machinery industries utilizing specialized forming fluids, positions the market for sustained expansion as manufacturers prioritize sustainable formulations and digitalized fluid management systems for demanding metalworking applications.

The metalworking fluids market in China is estimated to experience significant and promising growth from 2026 to 2035.

- Asia Pacific is the fastest-growing region in the market and includes China, India, Japan, South Korea, and Southeast Asian nations. China remains the most essential growth driver, increasingly driven by massive automotive production capacity representing the world's largest vehicle manufacturing base generating enormous removal fluids consumption, explosive electric vehicle manufacturing expansion requiring specialized fluids for aluminum battery housing machining and electric motor component fabrication, and expanding aerospace component manufacturing capacity for commercial aircraft programs. The country is experiencing both increased domestic metalworking fluids production from FUCHS Petrolub SE, TotalEnergies, and local manufacturers and rising consumption across automotive machining, aerospace fabrication, and construction machinery production, thus becoming the dominant regional player.

The metalworking fluids market in Saudi Arabia is estimated to experience significant and promising growth from 2026 to 2035.

- The metalworking fluids industry keeps steadily growing in the Middle East and Africa catered by expanding manufacturing diversification initiatives, massive infrastructure construction projects requiring machinery fabrication and metal forming operations, and developing aerospace maintenance, repair, and overhaul (MRO) facilities. Development of integrated manufacturing complexes, mega infrastructure initiatives, and industrial diversification drives demand for metalworking fluids across the region. In Saudi Arabia, Vision 2030 manufacturing localization programs promoting domestic automotive component production and machinery fabrication, expanding aerospace MRO capabilities consuming high-performance removal fluids, and emerging metal fabrication capacity drive increased metalworking fluids adoption for automotive parts machining, aerospace component maintenance, and construction equipment manufacturing supporting the Kingdom's economic diversification beyond oil production.

Brazil is estimated to experience significant and promising growth from 2026 to 2035.

- Brazil is contributing to the metalworking fluids market in Latin America owing to its expanding automotive manufacturing sector producing passenger vehicles and commercial trucks, domestic aerospace industry anchored by Embraer aircraft production consuming specialized fluids for aluminum aerospace alloy machining, and growing machinery manufacturing base for agricultural equipment and construction machinery. With Brazil's automotive production accelerating and demand for metalworking fluids in engine component machining and transmission manufacturing, aerospace component fabrication for regional jet production, and forming fluids for agricultural machinery stamping growing steadily, particularly in São Paulo automotive corridor and Rio de Janeiro metropolitan region, the market shows promising potential. Industries maintain growth trends with increasing adoption of semi-synthetic and synthetic formulations, supported by Shell, BP Castrol, and Petron Corporation.

Metalworking Fluids Market Share

Metalworking fluids markets are moderately consolidated, with players such as Quaker Houghton, FUCHS Petrolub SE, ExxonMobil, Shell (Shell Lubricants), and BP Castrol collectively accounting for 48% share of global supply in 2025, supported by their comprehensive product portfolios, global manufacturing footprints, and long-term relationships with automotive OEMs, aerospace manufacturers, and machinery producers.

- Metalworking fluids producers are actively engaged in formulation optimization and R&D to improve lubricity characteristics, extend sump life, enhance biodegradability, and reduce hazardous substance content including boron, formaldehyde, and chlorinated additives. Continuous innovations in synthetic base stock technology, bio-based ester formulations, extreme pressure additive packages, and emulsion stability enable manufacturers to meet specifications for high-speed machining, titanium aerospace alloy processing, aluminum automotive applications, and precision grinding operations, supported by advanced testing including tribology analysis, bacterial resistance testing, and tool life validation.

- Through strategic collaborations with machine tool manufacturers, automotive OEMs, aerospace primes, and industrial equipment builders, suppliers strengthen market positioning and demand stability. These partnerships support co-development of application-specific formulations, secure long-term supply agreements with technical service commitments, and enable integration of digital fluid monitoring systems across manufacturing operations, improving operational efficiency while supporting regulatory compliance including REACH, biocide regulations, and workplace safety initiatives for sustainable metalworking practices.

Metalworking Fluids Market Companies

Major players operating in the metalworking fluids industry are:

- Quaker Houghton

- FUCHS Petrolub SE

- ExxonMobil

- Shell (Shell Lubricants)

- BP Castrol

- Chevron (Caltex)

- TotalEnergies

- Idemitsu Kosan

- Yushiro Chemical

- Blaser Swisslube

- Master Fluid Solutions

- Milacron (Cimcool)

- Oemeta Chemische Werke

- Petron Corporation

- Phoenix Petroleum Philippines

Quaker Houghton is a global leader in industrial process fluids and metalworking solutions, headquartered in Conshohocken, Pennsylvania. The company offers comprehensive metalworking fluid portfolios including cutting fluids, grinding fluids, forming lubricants, heat treatment fluids, and corrosion preventives across soluble oil, semi-synthetic, synthetic, and neat oil formulations. Serving automotive, aerospace, steel, aluminum, mining, and general manufacturing sectors worldwide, Quaker Houghton emphasizes technical service capabilities, on-site fluid management programs, application-specific formulation development, and digital monitoring solutions. The company operates manufacturing facilities, technical centers, and service operations across North America, Europe, Asia-Pacific, and Latin America, providing localized support with global R&D capabilities and instrumented machining test facilities for product development and customer application optimization.

FUCHS Petrolub SE is the world's largest independent lubricant manufacturer, headquartered in Mannheim, Germany, operating across multiple countries with extensive production and technical service infrastructure globally. The company offers comprehensive metalworking fluid portfolios including water-miscible coolants, neat cutting oils, semi-synthetic and synthetic fluids, forming lubricants, quenchants, corrosion preventives, and minimum quantity lubrication products. Serving automotive, aerospace, medical technology, semiconductor, machinery manufacturing, and general metalworking sectors, FUCHS emphasizes technology leadership, application-specific solutions, and sustainability through bio-based formulations and circular economy initiatives. The company provides extensive OEM approvals, digital fluid management platforms, on-site technical services, and integrated lifecycle support combining products with monitoring, analytics, and fluid management programs across its global operating network.

ExxonMobil, through its industrial lubricants division and chemical specialty fluids operations, is one of the world's largest integrated manufacturers of lubricants, base stocks, and specialty hydrocarbon fluids with global production and distribution capabilities. The company offers metalworking fluids including water-soluble cutting fluids, hydrocarbon cooling and lubrication fluids, dearomatized solvents, synthetic isoparaffins for forming and rust prevention, and produces synthetic base stocks and mineral base oils supporting global metalworking fluid formulation. Serving automotive, aerospace, general machining, aluminum processing, and metal forming industries worldwide, ExxonMobil emphasizes high-performance formulations, technical application support, and global distribution through authorized dealer networks. The company operates major base oil production facilities and maintains extensive technical service capabilities supporting metalworking operations across diverse manufacturing sectors.

Shell Lubricants is a leading global lubricants supplier offering comprehensive industrial and metalworking solutions through its worldwide manufacturing, distribution, and technical service network. The company provides metalworking-related products including slideway oils for machine tools, hydraulic fluids, bearing and circulating oils, process oils, forming fluids, corrosion preventives, and specialty metalworking formulations. Serving manufacturing, automotive components, metalworking, aerospace, and industrial sectors globally, Shell emphasizes advanced technology including gas-to-liquids derived products for enhanced purity, sustainability initiatives including recycled-content formulations and biodegradable ranges, and comprehensive technical services. The company offers oil condition monitoring platforms, product selection tools, extensive OEM approvals, and integrated fluid management solutions supporting customers across diverse metalworking applications and geographic markets worldwide.

Metalworking fluids Industry News

- In July 2024, Quaker Houghton, a global supplier of industrial process fluids, has broken ground on a new state-of-the-art manufacturing facility in Zhangjiagang, China. The project aims to expand production capacity and strengthen the company’s supply chain across the Asia-Pacific region. The facility will integrate advanced manufacturing technologies with established safety and operational standards and is expected to become operational by the second quarter of 2026.

- In December 2025, Halocarbon has launched three advanced metalworking fluid formulations under its InfinX product line, now available through the company’s e-commerce platform. Designed for compatibility with standard MQL and conventional coolant delivery systems, the fluids integrate easily into existing CNC operations. Targeting high-precision industries such as aerospace, defense, nuclear energy, medical devices, and high-performance automotive, the products support machining of difficult-to-process metals.

The metalworking fluids market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million and volume in terms of Kilo Tons from 2022–2035 for the following segments:

Market, By Product

- Neat oil

- Soluble oil

- Semi-synthetic fluid

- Synthetic fluid

Market, By Application

- Removal fluids

- Forming fluids

- Protecting fluids

- Treating fluids

Market, By End Use

- Automotive

- Aerospace

- Construction

- Electrical & power

- Agriculture

- Marine

- Healthcare

- Others

The above information is provided for the following regions and countries:

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East & Africa

Frequently Asked Question(FAQ) :

Who are the key players in the metalworking fluids industry?

Key players include Quaker Houghton, FUCHS Petrolub SE, ExxonMobil, Shell (Shell Lubricants), BP Castrol, Chevron, TotalEnergies, Idemitsu Kosan, and Blaser Swisslube, focusing on formulation innovation, technical services, and global expansion.

What was the size of the U.S. metalworking fluids market in 2025?

The U.S. market accounted for USD 2.6 billion in 2025, supported by strong demand from automotive manufacturing, aerospace component production, and advanced machining operations across the country.

Which end-use industry leads the metalworking fluids market?

The automotive industry led the metalworking fluids industry with approximately 45.6% share in 2025. Extensive machining, forming, and surface treatment operations in vehicle and component manufacturing continue to drive strong fluid consumption.

What are the key trends in the metalworking fluids industry?

Key trends include development of bio-based and sustainable formulations, adoption of advanced synthetic fluids, integration of digital fluid management systems, and rising demand for high-performance fluids supporting CNC and high-speed machining operations.

What is the growth outlook for the synthetic fluids segment from 2026 to 2035?

The synthetic fluids segment is projected to grow at a CAGR of 7.3% from 2026 to 2035. Growth is supported by increasing demand for high-speed machining, extended sump life, and superior performance in aerospace and precision manufacturing applications.

Which product segment dominated the metalworking fluids industry in 2025?

Soluble oil dominated the market in 2025, accounting for approximately 40.3% share. Its leadership is driven by balanced lubrication and cooling performance, cost-effectiveness, and widespread use across general machining operations.

What was the largest application segment in the metalworking fluids market in 2025?

Removal fluids accounted for around 48.5% of the market in 2025, making them the largest application segment. High demand from cutting, grinding, drilling, and turning operations across automotive and aerospace manufacturing is driving segment dominance.

What is the metalworking fluids market size in 2025?

The market size for metalworking fluids is valued at USD 13.6 billion in 2025. Strong demand from automotive manufacturing, machinery production, and aerospace fabrication is supporting steady market expansion.

What is the market size of the metalworking fluids industry in 2026?

The market size for metalworking fluids reached USD 14.3 billion in 2026, reflecting consistent growth driven by rising machining and metal fabrication activities globally.

What is the projected value of the metalworking fluids market by 2035?

The market size for metalworking fluids is expected to reach USD 25.7 billion by 2035, growing at a CAGR of 6.7%. Expansion is fueled by advanced machining technologies, automotive production growth, and increasing adoption of high-performance and sustainable fluid formulations.

Metalworking Fluids Market Scope

Related Reports