Authors:

Preeti Wadhwani, Satyam Jaiswal

Download free PDF

Europe Cloud Computing Market Size & Share 2026-2035

Report ID: GMI2902

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Europe Cloud Computing Market

Get a free sample of this report

Get a free sample of this report Europe Cloud Computing Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

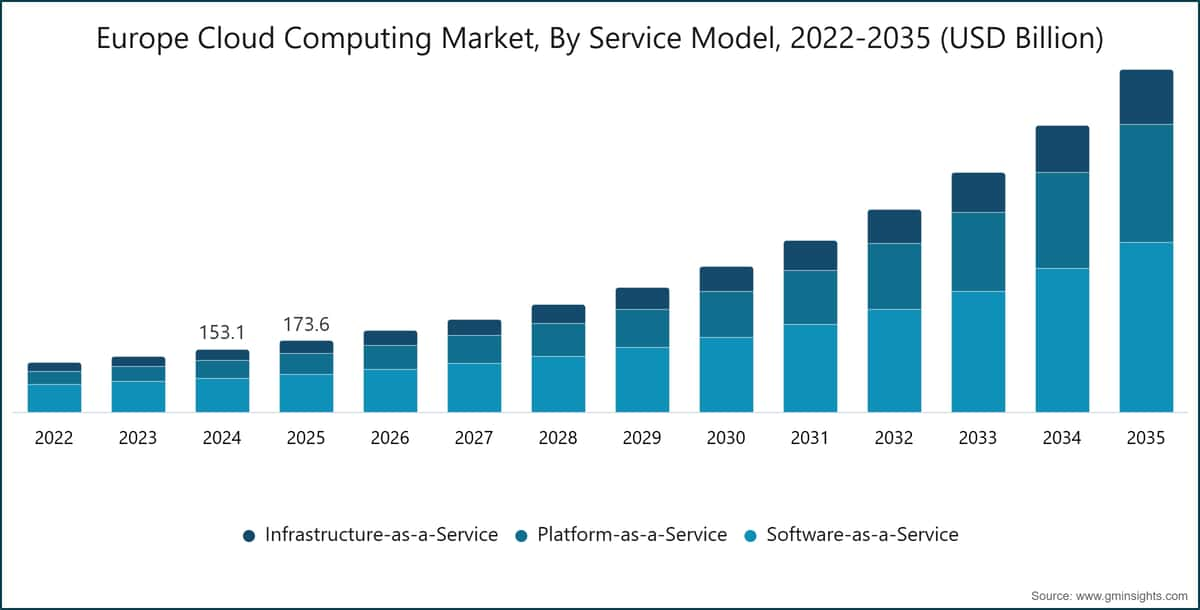

Europe Cloud Computing Market Size

The Europe cloud computing market was valued at USD 173.6 billion in 2025, spanning software, platform, and infrastructure services across public, hybrid, and private deployment models. The market is projected to reach USD 837 billion by 2035, expanding at a 17.4% CAGR during 2026–2035. This growth profile is according to latest report published by Global Market Insights Inc.

Europe Cloud Computing Market Key Takeaways

Market Size & Growth

Regional Dominance

Key Market Drivers

Challenges

Opportunity

Key Players

Enterprise demand is moving beyond storage and productivity workloads into AI, analytics, regulated data processing, and cloud-native application development. Western Europe remains the largest sub-region, while Northern Europe is advancing fastest as digital maturity, public-sector cloud procurement, and sovereign infrastructure requirements converge.

Key Drivers

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Increasing digital transformation initiatives

+4.5%

Western Europe, Northern Europe

Medium term (2-4 years)

Demand for scalable and cost-efficient IT infrastructure

+4%

All sub-regions

Short term (≤ 2 years)

Growing adoption of cloud-based business applications

+3.5%

Western Europe, Eastern Europe

Medium term (2-4 years)

Rising data storage and analytics requirements

+3.2%

All sub-regions

Long term (≥ 4 years)

Increasing digital transformation initiatives

Enterprise digital transformation has shifted from a sequence of isolated IT projects to a capital allocation priority across European industries. Eurostat reported that 45.2% of EU enterprises with at least 10 employees used cloud computing services in 2024, up from 36% in 2021, confirming that adoption has moved well beyond early migration cycles.[1]Eurostat, https://ec.europa.eu/eurostat SAP S/4HANA Cloud, SAP Business Technology Platform, Microsoft Dynamics 365, and Workday Financial Management are central to this shift because European enterprises are modernizing core finance, HR, procurement, and operations platforms rather than only replacing peripheral workloads. The resulting demand supports both SaaS renewal intensity and platform-level consumption for integration, analytics, and application development.

Demand for scalable and cost-efficient IT infrastructure

Cloud economics have become more compelling as hardware refresh cycles, cybersecurity expenditure, and internal data center energy costs rise. Consumption-based pricing allows enterprises to reallocate capital expenditure toward operating expenditure, while public and hybrid cloud architectures reduce the need to overprovision compute capacity for peak demand. OECD analysis of digital economy investment across European member states points to a sustained shift in enterprise ICT spending toward cloud infrastructure during 2020–2024.[2]Organisation for Economic Co-operation and Development, https://www.oecd.org The impact is strongest among Small and Medium Enterprises, which are projected to grow at a 20.1% CAGR through 2035 as accessible SaaS and IaaS offerings bring enterprise-grade capability into the mid-market.

Growing adoption of cloud-based business applications

Software-as-a-Service remains the largest service layer in the Europe cloud computing market, generating USD 92.7 billion in 2025 and representing 53.4% of total cloud spend. Salesforce Sales Cloud, Microsoft Dynamics 365, SAP SuccessFactors, Workday HCM, and ServiceNow Platform are embedded across European enterprises, creating recurring subscription revenue and high switching costs. The underlying driver is not just application replacement; enterprises are adding AI copilots, analytics modules, integration services, and workflow automation on top of existing SaaS contracts. That expands average revenue per user even when headcount growth is moderate.

Rising data storage and analytics requirements

European enterprises are producing and retaining more operational, customer, regulatory, and machine-generated data than legacy on-premise environments can process efficiently. Manufacturing plants generate continuous IoT streams from connected production lines, while banks and insurers manage structured data retention under EMIR, MiFID II, Basel IV, and DORA-aligned risk processes. The AI, ML & Analytics application segment is forecast to grow from USD 24.3 billion in 2025 to USD 202.6 billion by 2035, at a 23.8% CAGR. Cloud infrastructure is becoming the default compute layer for model training, inference, data warehousing, governed data sharing, and real-time analytics.

Key Challenges

Challenge

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Data security and regulatory compliance concerns

-2.8%

All sub-regions, most restrictive in Western and Northern Europe

Medium term (2-4 years)

Cloud migration and multi-cloud management complexity

-2%

All sub-regions

Short term (≤ 2 years)

Data security and regulatory compliance concerns

Data sovereignty requirements, GDPR transfer restrictions, DORA obligations for financial institutions, and the NIS2 Directive for critical infrastructure operators create a compliance burden that slows migration and raises deployment costs. ENISA documented a 22% increase in cloud-specific security incidents in Europe between 2022 and 2024, making cloud infrastructure a more visible target for ransomware and state-linked threat actors.[3]European Union Agency for Cybersecurity, https://www.enisa.europa.eu Hyperscale’s are responding with EU-resident processing guarantees, sovereign product lines and third-party audit certifications, but certification uncertainty under EUCS High continues to add procurement friction. The mitigation path is clear: regulated buyers increasingly require ISO 27001, BSI C5, SecNumCloud, EU data residency and cloud key-management controls before production workloads move.

Cloud migration and multi-cloud management complexity

Multi-cloud operating models introduce complexity in cost governance, identity management, policy enforcement, observability, and application performance management. Enterprises running workloads across Azure, Google Cloud, AWS, and on-premise Kubernetes clusters often discover that abstraction reduces lock-in but increases operating burden. IBM Turbonomic, Cloud Health by VMware, and Apptio Cloud ability are gaining relevance as FinOps and governance tools because European CIOs need spend control as much as technical scalability. The challenge is especially acute in mid-market Eastern Europe, where cloud architecture skills are improving but remain thinner than in London, Frankfurt, Paris, Amsterdam and Stockholm.

Europe Cloud Computing Market Trends

AI workloads are becoming the most powerful incremental demand source in the Europe market. The AI, ML & Analytics application segment is projected to grow from USD 24.3 billion in 2025 to USD 202.6 billion by 2035, at a 23.8% CAGR. This growth rate is nearly 6 percentage points above the overall market CAGR, showing that AI is not merely another application category. It is changing infrastructure requirements, with enterprises demanding GPU availability, data pipeline integration, model governance, inference cost controls, and secure access to proprietary datasets.

Microsoft Azure OpenAI Service has become a primary enterprise entry point for generative AI deployment because it combines large language model access with Azure security, identity, compliance, and procurement structures already accepted by European IT teams. Google Vertex AI is gaining traction among data-science-led organizations using model training, fine-tuning, and managed inference. SAP Business AI, embedded within SAP Business Technology Platform, is especially relevant for European ERP customers because AI-assisted financial close, procurement analytics, and supply chain exception management can be deployed against existing SAP process data. IEEE Spectrum has documented the compute intensity of generative AI workloads, including the energy and infrastructure pressure created by model training and inference at scale.[4]IEEE Spectrum, https://spectrum.ieee.org

In our Q1 2026 interviews with 42 cloud strategy leaders across Germany, France, the United Kingdom, the Netherlands, and Sweden, production generative-AI use was moving out of controlled pilots and into customer service, code generation, document processing, and internal knowledge-search workflows. The interviews pointed to a practical constraint: enterprises are not only choosing models; they are choosing cloud operating environments that can govern model access, track data lineage, and keep sensitive prompts within approved regions. The timeline is near term for customer-service and developer-productivity use cases, medium term for AI-supported ERP and supply chain planning, and longer term for highly regulated model deployment in financial risk and healthcare diagnostics.

Hybrid cloud is consolidating as the enterprise-preferred architecture for large European organizations. The segment accounted for USD 41.4 billion in 2025, or 23.9% of deployment model spend, and is expected to grow at an 18.3% CAGR through 2035. Public cloud grows at a similar 18.2% CAGR, but hybrid cloud’s role is distinct: it lets enterprises keep sensitive data or latency-critical workloads under tighter control while using public cloud for scalable compute, analytics, AI, and collaboration services. The architecture fits Europe because data protection, sectoral regulation, and national sovereignty expectations shape procurement more directly than in less regulated markets.

Azure Arc and Google Anthos are important platforms in this shift because they extend governance, policy control, container orchestration, and security management across on-premise, edge, and public cloud environments. AWS Outposts, Azure Stack Edge, and Google Distributed Cloud perform a similar role for workloads that need cloud capabilities closer to factories, branch sites, telecom networks, or regulated data stores. Volkswagen Group’s hybrid cloud use for vehicle software development, combining Azure services with controlled environments for over-the-air update pipelines, illustrates the model’s appeal in a high-complexity manufacturing setting. The market implication is clear: hybrid cloud is not a transitional compromise; it is becoming a durable architecture for regulated, operationally complex enterprises.

Edge computing is becoming a structural extension of European cloud architecture rather than a separate technology category. Manufacturing plants, telecom operators, smart city programs, and logistics networks increasingly need compute closer to data-generation points because latency, bandwidth cost, and data-residency controls limit full centralization. Deutsche Telekom’s multi-access edge computing deployments across German industrial parks provide a practical example, supporting low-latency industrial applications such as real-time quality inspection and production-line monitoring. GSMA analysis of telecom edge and 5G enterprise services supports the broader view that distributed compute will be tied closely to network modernization and industry digitization.[5]GSMA, https://www.gsma.com

Security & Compliance is a direct beneficiary of edge expansion, growing at an 18.5% CAGR. As workloads move closer to endpoints, enterprises need zero-trust policy enforcement, identity controls, logging, compliance reporting, and threat detection across a more distributed estate. That creates demand for cloud-delivered security platforms, managed detection, configuration monitoring, and data-loss prevention. The investment timeline is short to medium term in telecom and manufacturing, while public-sector smart city use cases should build more gradually as procurement cycles and interoperability requirements mature.

Sovereign cloud has moved from policy language into procurement practice. The EU Cloud Certification Scheme, developed by ENISA, establishes assurance tiers for cloud services, while EUCS High is particularly relevant for public administration and critical infrastructure because it emphasizes EU-resident operations, EU-based key management, and restrictions on non-EU staff access. Gaia-X also remains relevant as an industrial data initiative, particularly where cross-company data sharing requires trust, interoperability, and governance controls. European Parliament work on the EU Data Act has added another dimension by clarifying portability and switching obligations for cloud providers.[6]European Parliament, https://www.europarl.europa.eu

Several deployments show how this trend is materializing. OVH cloud’s SecNumCloud-certified Horizon platform serves French government and regulated customers. Microsoft Cloud for Sovereignty offers contractual EU data residency commitments for public sector clients. SAP EU Access restricts customer data operations to EU-resident personnel. Italy’s Polo Strategico Nazionale is one of the largest examples, consolidating 22,000 public administration data centers into a sovereign cloud environment operated by Leonardo and TIM Enterprise. The Government & Public Sector segment, valued at USD 12.3 billion in 2025, is projected to grow at an 18.8% CAGR through 2035 as these frameworks become embedded in procurement.

Europe Cloud Computing Market Analysis

By Service Model

Software-as-a-Service is the largest service model in the Europe cloud computing market, accounting for USD 92.7 billion in 2025, or 53.4% of total market value. The segment is projected to reach USD 415 billion by 2035 at a 16.5% CAGR, supported by CRM, HCM, ERP, collaboration, analytics, and workflow platforms. Salesforce Sales Cloud, Microsoft Dynamics 365, SAP SuccessFactors, Workday Human Capital Management, and ServiceNow Platform are core enterprise systems rather than discretionary software. AI modules such as Microsoft Copilot for Microsoft 365 and Salesforce Einstein GPT are expanding per-seat revenue within existing customer accounts. This makes SaaS growth less dependent on new customer acquisition alone.

Platform-as-a-Service is the fastest-growing service model, expanding at a 19.6% CAGR from USD 49.1 billion in 2025 to USD 286.5 billion by 2035. In our Q4 2025 discussions with 35 cloud architecture leads across Tier-1 European enterprises, PaaS and managed Kubernetes/serverless environments were repeatedly identified as the fastest-rising spend priority because internal development teams are building proprietary applications on cloud platforms. Azure Kubernetes Service, Google Cloud Run, AWS Lambda, and Red Hat OpenShift are central to that shift. Infrastructure-as-a-Service, valued at USD 31.8 billion in 2025, remains the foundational layer for compute, GPU capacity, storage, backup, and networking. Data center capacity constraints in Germany, the Netherlands, France, Ireland, and Sweden will influence IaaS pricing and availability through the 2026–2028 investment cycle.

By Deployment Model

Public cloud is the dominant deployment model, representing USD 100 billion in 2025 and 57.6% of European cloud spend. The segment is forecast to reach USD 519.2 billion by 2035 at an 18.2% CAGR, supported by shared infrastructure economics, hyperscaler AI investment, and broader availability of European cloud regions. AWS operates European regions across Frankfurt, Ireland, Paris, Stockholm, Milan, Zurich, and a dedicated EU Sovereign Cloud in Germany from 2025. Microsoft Azure maintains the broadest European regional presence among hyperscalers, with continued data center expansion through 2026. Google Cloud is strengthening residency coverage through regions in France, Poland, and other European markets.

Hybrid cloud generated USD 41.4 billion in 2025 and is growing at an 18.3% CAGR, marginally ahead of public cloud. Financial services, healthcare, manufacturing, public administration, and telecom operators use hybrid models because sensitive data, operational continuity, and latency-critical workloads often cannot move fully into multi-tenant public environments. Private cloud accounts for USD 32.1 billion and 18.5% share in 2025, but its 12.5% CAGR trails other deployment models. The second-order effect is pressure on HPE GreenLake, Dell APEX, and traditional private cloud providers to differentiate through hardware lifecycle management, edge deployment, and managed on-premise control rather than pure sovereignty messaging.

By Enterprise Size

Large enterprises accounted for USD 118.8 billion in 2025, representing 68.4% of the Europe cloud computing market. Their spending is anchored in multi-year ERP migrations, Microsoft enterprise agreements, SAP S/4HANA Cloud programs, Red Hat OpenShift deployments, and broad use of CRM, analytics, security, collaboration, and infrastructure services. Banks, manufacturers, retailers, telecom operators, and public sector institutions often run multi-cloud estates because they need resilience, negotiating flexibility, and best-of-breed capabilities. Financial Conduct Authority oversight in the United Kingdom and DORA requirements across the EU are reinforcing the need for exit planning, resilience testing, and third-party risk controls in cloud outsourcing.

Small and Medium Enterprises generated USD 54.8 billion in 2025 and are forecast to reach USD 334 billion by 2035 at a 20.1% CAGR. Their adoption curve is steeper because cloud subscriptions reduce the need for owned infrastructure and specialist internal IT resources. IONOS Cloud, Hetzner Online, OVHcloud, Scaleway, Aruba Cloud, and regional managed service providers are well positioned in this tier because SMEs often prioritize local support, transparent pricing, data residency, and packaged services. The SME opportunity is especially visible in Eastern Europe and Southern Europe, where cloud penetration remains lower than in Western Europe but EU digital funding, e-commerce growth, and IT services exports are accelerating demand.

By Application

AI, ML & Analytics is the fastest-growing application category, expanding at a 23.8% CAGR from USD 24.3 billion in 2025 to USD 202.6 billion by 2035. The segment includes model training, inference, data warehousing, analytics, governed data sharing, and AI-assisted business process automation. Google Vertex AI, Azure OpenAI Service, SAP Business AI, Snowflake Data Cloud, BigQuery, and Looker Studio are among the most relevant platforms because they combine data management with model or analytics services. Demand is strongest where enterprises already hold large structured datasets, including banking, retail, telecommunications, manufacturing, and public administration.

Security & Compliance is the second-highest-growth application category at an 18.5% CAGR. The driver is not only cyber risk; it is the regulatory operating model surrounding GDPR, DORA, NIS2, EUCS, SecNumCloud, BSI C5, and cloud outsourcing rules. Managed identity, encryption, zero-trust controls, audit logging, policy-as-code, cloud security posture management, and data-loss prevention are becoming baseline requirements. CRM, HCM, ERP, collaboration, and data storage remain large application pools, with Salesforce Sales Cloud, Workday HCM, SAP S/4HANA Cloud, ServiceNow Platform, Microsoft 365, and Snowflake Data Cloud anchoring enterprise consumption.

By End-Use Industry Vertical

BFSI is the largest end-use vertical, generating USD 31.8 billion in 2025. Banks, insurers, asset managers, and payment firms use cloud for digital banking, risk analytics, fraud detection, regulatory reporting, data warehousing, customer engagement, and resilience planning. DORA is changing vendor due diligence because institutions must demonstrate operational resilience, incident reporting discipline, and oversight of critical third-party ICT providers. AWS EU Sovereign Cloud, Microsoft Cloud for Sovereignty, IBM Red Hat OpenShift, and Google Cloud analytics services are relevant here because financial institutions need elasticity and compliance in the same architecture.

Manufacturing generated USD 27.9 billion in 2025, while Retail & E-commerce reached USD 24.8 billion. Manufacturers use cloud for connected production, digital twins, quality inspection, supply chain planning, and SAP-centered ERP modernization. Retailers use cloud for omnichannel commerce, personalization, inventory management, customer data platforms, and demand forecasting. Government & Public Sector generated USD 12.3 billion in 2025 and is growing at an 18.8% CAGR, supported by sovereign cloud procurement. Education is the fastest-growing named vertical at a 20.4% CAGR, while IT & Telecom grows at 19% as operators combine network modernization with edge computing and cloud-native service delivery.

By Region

Northern Europe Cloud Computing Market Trends

The Northern Europe market was valued at USD 29.7 billion in 2025 and is forecast to reach USD 159.4 billion by 2035 at an 18.6% CAGR, the fastest sub-regional growth rate in Europe. The United Kingdom is the most dynamic national market, generating USD 13.9 billion in 2025 and expanding at a 19.8% CAGR. The UK Government’s G-Cloud 14 framework, administered by the Crown Commercial Service, qualifies more than 40,000 cloud services for public sector purchase without separate tendering, materially reducing procurement friction. Scandinavian markets are also advancing because Sweden and Finland combine high digital maturity with growing attention to EUCS-aligned sovereign procurement. In our Q1 2026 survey of 54 public-sector cloud procurement officials across the United Kingdom, Germany, France, Italy, Poland, Sweden, and Finland, certification readiness and EU-resident operations were cited as tender-shortlisting considerations more often than headline infrastructure pricing.

Western Europe Cloud Computing Market Trends

The Western Europe market is the largest sub-region, reaching USD 81.9 billion in 2025 and representing 47.2% of total European cloud spend. Germany anchors the sub-region at USD 43.5 billion in 2025, equal to 25.1% of the European total, with demand shaped by SAP-centered ERP modernization, Industrie 4.0 manufacturing digitization, and BSI C5 compliance requirements. France, the Netherlands, and Belgium form the Rest of Western Europe cluster, which is advancing at an 18% CAGR. France’s SecNumCloud framework, operated by ANSSI, has strengthened demand for OVHcloud, Capgemini, and other providers with sovereign cloud capabilities. Google Cloud confirmed its third French cloud region in 2024, improving data residency coverage for public sector and financial services clients operating under French sovereignty expectations.

Eastern Europe Cloud Computing Market Trends

The Eastern Europe market generated USD 40.2 billion in 2025 and is projected to reach USD 201.6 billion by 2035 at a 17.8% CAGR. Poland is the anchor, generating USD 10.2 billion in 2025 and growing at a 16.1% CAGR, supported by financial services digitization, advanced manufacturing, and a large IT services export sector. Google Cloud and Microsoft Azure announced dedicated Polish data center regions during 2023–2024, reducing dependence on German and Irish cloud regions for data residency. The Polish Financial Supervision Authority’s cloud guidance has increased the importance of local infrastructure, governance controls, and documented exit plans for regulated financial workloads. Czech Republic, Hungary, Romania, and the Baltic states are benefiting from EU Digital Europe Programme and Cohesion Fund support for SME digitization and cloud infrastructure investment.

Southern Europe Cloud Computing Market Trends

The Southern Europe market reached USD 21.7 billion in 2025 and is forecast to reach USD 98.5 billion by 2035 at a 16.7% CAGR. Italy is the dominant national market at USD 14.3 billion in 2025, growing at a 16.4% CAGR. The Polo Strategico Nazionale initiative is central to Italian demand because it is consolidating 22,000 public administration data centers into a sovereign cloud environment operated by Leonardo and TIM Enterprise, with capacity to support 80% of Italian public administration workloads. Spain, Portugal, and Greece form the Rest of Southern Europe cluster, growing at a 17.2% CAGR. Spain’s España Digital 2026 strategy and Telefónica Tech’s AI-native cloud platform expansion are supporting enterprise and SME cloud adoption across the Iberian Peninsula.

Europe Cloud Computing Market Share

Microsoft Azure holds the largest share of the Europe market at 15.2% in 2025, translating to approximately USD 26.4 billion in European revenue across Azure infrastructure, Microsoft 365, Dynamics 365, and Azure OpenAI Service. Microsoft’s position is reinforced by procurement consolidation: large enterprises often buy productivity software, cloud infrastructure, AI tools, endpoint security, and business applications under enterprise agreement structures. That creates renewal advantages and lowers the friction of adding Copilot or Azure OpenAI Service to existing accounts. Microsoft’s EUR 4.3 billion cloud and AI infrastructure investment across Germany, announced in April 2025, also directly addresses data residency and capacity requirements in Europe’s largest national market.

Google Cloud holds 12.1%, with an edge in AI, analytics, data warehousing, and Kubernetes-native development. Vertex AI, BigQuery, Looker Studio, and Google Kubernetes Engine make Google Cloud especially competitive in accounts where machine learning and governed analytics are the primary workloads. AWS holds 10.8%, supported by a broad technical portfolio covering Lambda, EKS, Aurora, DynamoDB, RDS, and cloud-native developer services. The 2025 launch of AWS EU Sovereign Cloud in Germany widened AWS’s addressable market in regulated public sector, automotive, and financial services workloads where sovereignty requirements previously constrained adoption.

SAP SE commands 7.2% of the market, reflecting the depth of SAP’s installed base across European enterprises. More than 80% of DAX40 companies operate SAP systems, and the migration toward SAP S/4HANA Cloud and SAP Business Technology Platform is one of the largest structured enterprise cloud transitions in the region. IBM holds 5.8%, with Red Hat OpenShift acting as a differentiated hybrid cloud platform in regulated industries. IBM Watsonx and IBM Consulting add AI and transformation-service layers that pure-infrastructure providers do not offer in the same form. Salesforce holds 4.5%, while Snowflake’s 0.4% headline share understates its influence on cross-cloud data strategy and governed analytics.

In our Q2 2025 expert panel with eight senior cloud infrastructure executives, discussion converged on a single competitive issue: EUCS High certification timing will heavily influence public sector and critical infrastructure cloud procurement during 2026–2027. That does not mean hyperscalers lose share. It means Microsoft, AWS, Google Cloud, Oracle, SAP, IBM, and regional European providers must prove operational sovereignty, auditability, key management discipline, and local control at the procurement stage.

The top five players collectively hold 51.1% of the market, indicating moderate concentration. The remaining 44% is distributed across Salesforce, Snowflake, Oracle, Workday, ServiceNow, OVHcloud, Deutsche Telekom/T-Systems, IONOS Cloud, Hetzner Online, Scaleway, Orange Business, Telefónica Tech, Aruba Cloud, Capgemini, STACKIT, and other specialists. Regional providers will not displace hyperscalers in commodity compute at scale, but they can win regulated workloads, public sector tenders, SME accounts, and sovereignty-sensitive customers. M&A and partnership activity should therefore concentrate around sovereign hosting, managed security, FinOps, cloud migration services, and data governance capabilities rather than generic IaaS capacity alone.

Europe Cloud Computing Market Companies

Major players operating in the Europe cloud computing industry are:

Major players operating in the Europe market are: Microsoft (Azure), Amazon Web Services (AWS), Google Cloud, SAP SE, Salesforce, Oracle, IBM (Cloud + Red Hat), Workday, ServiceNow, Snowflake, OVHcloud, Deutsche Telekom / T-Systems, Hetzner Online, IONOS Cloud, Scaleway, Orange Business, Telefónica Tech, Aruba Cloud, Capgemini, and STACKIT.

Microsoft (Azure) is the largest cloud services provider in Europe by market share. Its portfolio spans Azure IaaS/PaaS, Microsoft 365, Dynamics 365, Azure OpenAI Service, Microsoft Copilot for Microsoft 365, and Cloud for Sovereignty. The RISE with SAP partnership channels ERP migration spend through Azure infrastructure, while enterprise agreements help Microsoft bundle productivity, infrastructure, security, and AI services into renewal cycles.

Amazon Web Services (AWS) competes through technical portfolio breadth and mature cloud-native services. Lambda, EKS, Aurora, DynamoDB, RDS, Outposts, and AWS EU Sovereign Cloud support workloads ranging from startups to regulated enterprises. The Germany-based EU Sovereign Cloud is strategically important because it targets German public sector, automotive, and financial services clients with EU-resident operations and local access controls.

Google Cloud differentiates on AI, data analytics, and Kubernetes. Vertex AI supports model training, fine-tuning, and inference, while BigQuery and Looker Studio anchor data warehousing and business intelligence. Google Anthos and Google Kubernetes Engine remain relevant for enterprises standardizing on containerized application development and multi-cloud governance.

SAP SE is central to European enterprise cloud migration because its ERP systems sit inside finance, procurement, HR, manufacturing, and supply chain processes. SAP S/4HANA Cloud, RISE with SAP, SAP Business Technology Platform, SAP SuccessFactors, and SAP EU Access give the company a strong position in application-led cloud modernization. EU Access is especially important for regulated clients because it restricts customer data operations to EU-resident personnel.

Salesforce provides core CRM, service, marketing, integration, and analytics capabilities through Sales Cloud, Service Cloud, Marketing Cloud, MuleSoft, Tableau, and Salesforce Platform. Salesforce Einstein GPT is the company’s primary AI expansion vector across European accounts. Its strength lies in front-office transformation, customer data, and workflow automation.

Oracle competes through Oracle Cloud Infrastructure and Oracle Fusion Cloud ERP/HCM. Existing Oracle Database licensees provide a structured migration base for OCI, while Oracle’s EU Sovereign Cloud supports public sector and healthcare workloads in countries such as France and Spain. The company’s position is strongest where database modernization and ERP/HCM cloud migration are linked.

IBM (Cloud + Red Hat) relies on Red Hat OpenShift, IBM Watsonx and IBM Consulting. OpenShift is a key enterprise Kubernetes platform across regulated industries, while Watsonx supports AI development and deployment. IBM Consulting gives IBM an implementation layer for financial services, telecom, government, and hybrid cloud transformation programs.

Workday and ServiceNow are specialized SaaS leaders. Workday HCM and Workday Financial Management serve large European enterprises standardizing HR and finance processes. ServiceNow Platform is a benchmark for IT service management, workflow automation, and enterprise service delivery, and the company’s dedicated Frankfurt data center, opened in 2025, strengthens GDPR-aligned EU data residency for European customers.

Snowflake operates the Snowflake Data Cloud for governed analytics, cross-cloud data sharing, and AI-ready enterprise data management. Its European AI Data Cloud launch in 2024, with model hub integration in Frankfurt and Amsterdam, supports European enterprises seeking to train and serve AI models on Snowflake-resident data without cross-border transfer. This makes Snowflake strategically important even with a small direct market share.

Regional European providers form a critical second tier. OVHcloud serves sovereignty-sensitive customers through SecNumCloud-certified infrastructure. Deutsche Telekom / T-Systems combines cloud, connectivity, and German public-sector relationships. IONOS Cloud and Hetzner Online compete on mid-market IaaS pricing and data residency. Scaleway, Aruba Cloud, Orange Business, and Telefónica Tech serve developer, SME, telecom-integrated, and national-market needs. Capgemini and Accenture provide cloud integration and migration services, while STACKIT, backed by Schwarz Group, is expanding as a European sovereign cloud provider anchored by the Lidl/Kaufland parent ecosystem.

15.2% Market Share

Collective Market Share in 2025 is 51.1%

Europe Cloud Computing Industry News

Europe Cloud Computing Market Concentration Score

The Europe cloud computing market has a concentration score of 6.5 out of 10 because the top five providers hold 51.1% of 2025 revenue, yet nearly half of the market remains available to SaaS specialists, sovereign cloud providers, telecom cloud operators, regional IaaS firms, and systems integrators.

The Europe cloud computing market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Service Model

Market, By Deployment Model

Market, By Application

Market, By Organization Size

Market, By End-Use Industry

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Service Model, 2022 - 2035 ($Mn)

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2022 - 2035 ($Mn)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

Chapter 8 Market Estimates & Forecast, By Organization Size, 2022 - 2035 ($Mn)

Chapter 9 Market Estimates & Forecast, By End-Use Industry, 2022 - 2035 ($Mn)

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

Chapter 11 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →